Date 24th August 2023.

Market Update – August 24 – NVDA posts stellar Q2 results; Stocks, Bonds, Metals rally on eve of Jackson Hole.

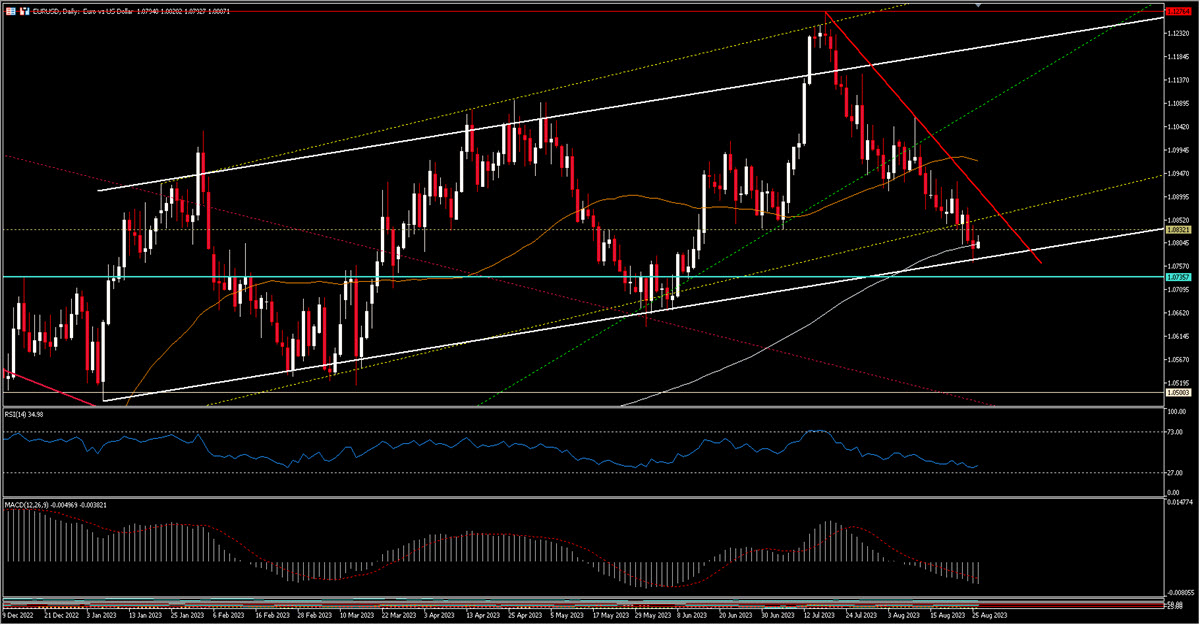

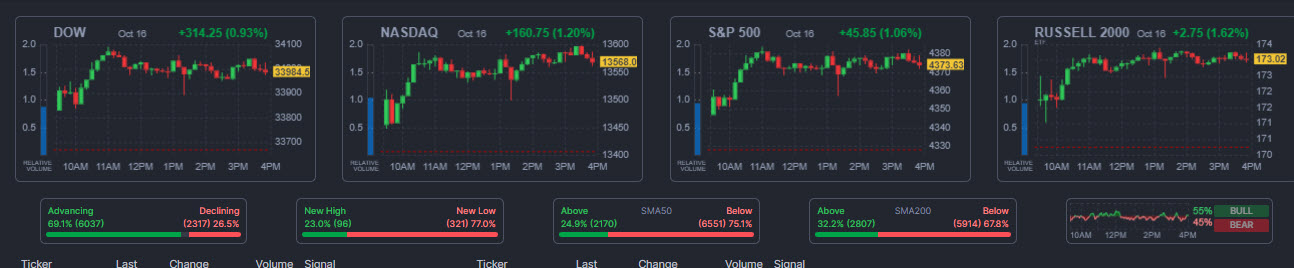

Let’s start with NVIDIA that after the close reported results of a stellar Q2 and topped analyst estimates both on Revenues ($13.51 billion vs $11.22 billion expected) and EPS ($2.70 vs $2.09). The company raised its forecast again and expects its Q3 revenues to climb to $16 billion, an increase of 170% y/y. Gains are driven by the data center business. In after hours trading the chip-maker rose 6.57% also driving up AMD (+4%) and TSMC (+3.1%). Indices added to this week rally despite weak PMIs data around the Developed Markets that instead weighted on local currencies: EUR, GBP and USD fell in this order during the day after lackluster readings. Interestingly, the EURUSD perfectly rebounded on its 200 MA.

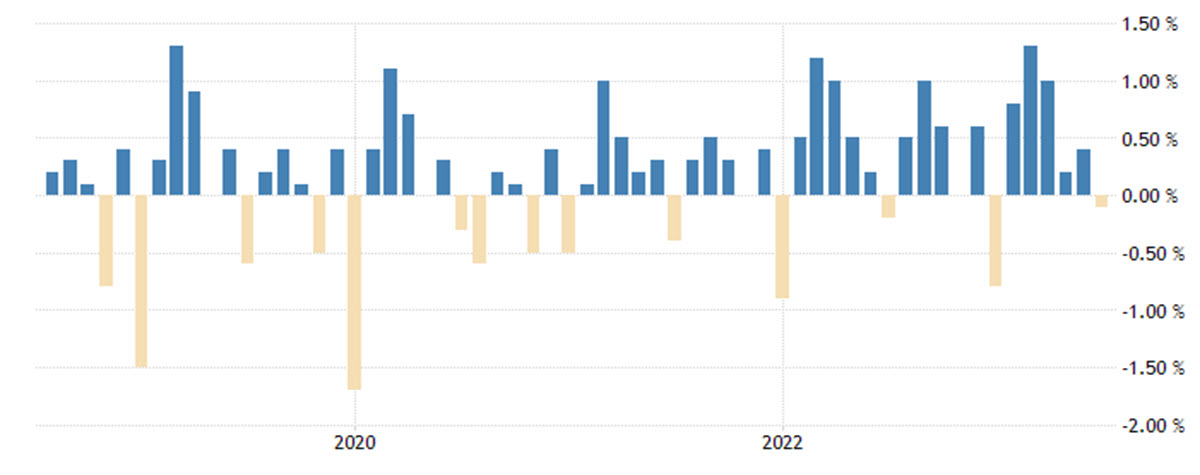

US 30y mortgage rate soared to 7.31% and this led to the lowest Mortgage applications since 1995: despite that, US new home sales rose in July. Bonds rallied around the world with the UK Gilt up 2.13% after traders repriced the terminal rate well below 6% and a narrow majority of economists polled by Reuters now believe the September hike to 5.5% will be the last one. German Bund gave up >10 bps and the 10y US T-note is 17bps off this week’s high. All of this gave wings to Gold, which touched $1921, and especially Silver, which rose 3.88%. Overnight, Asia joined the party and China50 rebounded strongly from near one-year lows.

US 30y mortgage rate soared to 7.31% and this led to the lowest Mortgage applications since 1995: despite that, US new home sales rose in July. Bonds rallied around the world with the UK Gilt up 2.13% after traders repriced the terminal rate well below 6% and a narrow majority of economists polled by Reuters now believe the September hike to 5.5% will be the last one. German Bund gave up >10 bps and the 10y US T-note is 17bps off this week’s high. All of this gave wings to Gold, which touched $1921, and especially Silver, which rose 3.88%. Overnight, Asia joined the party and China50 rebounded strongly from near one-year lows.

US Mortgage 30 Years Rate and Mortgage Applications

INTERESTING FX MOVER: USDIndex (-0.05% @ 103.28) pulled back after rising as high as 103.90 in what could be the test of the upper bound of a channel. It is trading above both the 50 and 200 MA and both RSI and MACD are positive and upward sloping.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Click HERE to READ more Market news.

Marco Turatti

Market Analyst

HFMarkets

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – August 24 – NVDA posts stellar Q2 results; Stocks, Bonds, Metals rally on eve of Jackson Hole.

Let’s start with NVIDIA that after the close reported results of a stellar Q2 and topped analyst estimates both on Revenues ($13.51 billion vs $11.22 billion expected) and EPS ($2.70 vs $2.09). The company raised its forecast again and expects its Q3 revenues to climb to $16 billion, an increase of 170% y/y. Gains are driven by the data center business. In after hours trading the chip-maker rose 6.57% also driving up AMD (+4%) and TSMC (+3.1%). Indices added to this week rally despite weak PMIs data around the Developed Markets that instead weighted on local currencies: EUR, GBP and USD fell in this order during the day after lackluster readings. Interestingly, the EURUSD perfectly rebounded on its 200 MA.

US 30y mortgage rate soared to 7.31% and this led to the lowest Mortgage applications since 1995: despite that, US new home sales rose in July. Bonds rallied around the world with the UK Gilt up 2.13% after traders repriced the terminal rate well below 6% and a narrow majority of economists polled by Reuters now believe the September hike to 5.5% will be the last one. German Bund gave up >10 bps and the 10y US T-note is 17bps off this week’s high. All of this gave wings to Gold, which touched $1921, and especially Silver, which rose 3.88%. Overnight, Asia joined the party and China50 rebounded strongly from near one-year lows.US Mortgage 30 Years Rate and Mortgage Applications

- FX – USDIndex -0.05% at 103.28, EURUSD flat at 1.0865 after falling as low as 1.0802 yesterday, GBPUSD -0.09% @ 1.2713 still between the recent 1.2615/1.2785 range, USDJPY back above 145 (breached yesterday).

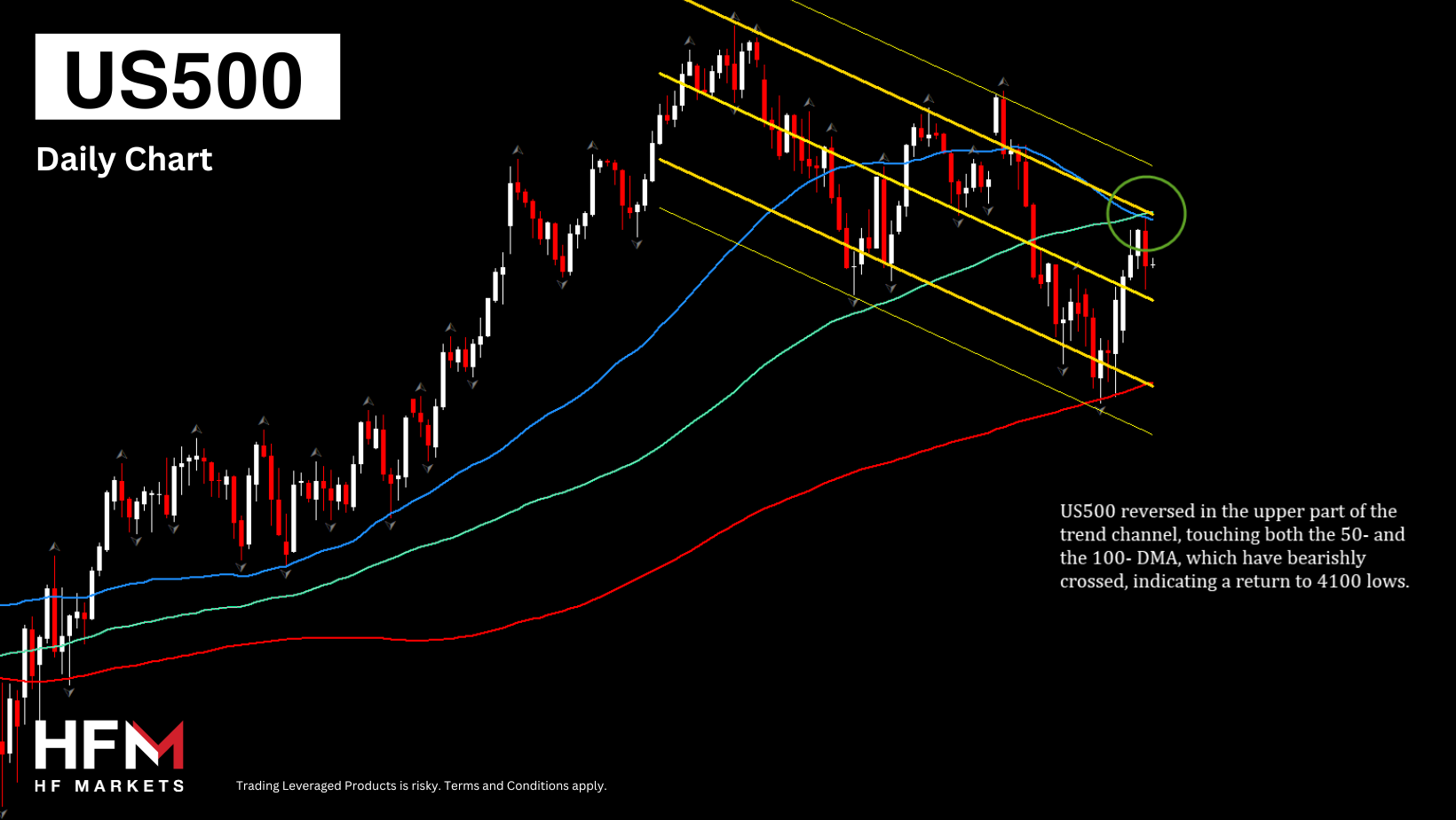

- Stocks – US Futures almost flat (-0.05% US30/+0.16% US100/+0.05% US500), EU Futures up 0.4%/0.6%; CHINA50 +1.42%, Hang Seng +1.91%, JPN225 +0.79%.

- Commodities – USOil is below $79 ($78.48 now) despite the bigger than expected drain from Oil Stocks (EIA data).

- Gold – holding at $1921, XAG consolidating at $24.23 after yesterday’s rally.

INTERESTING FX MOVER: USDIndex (-0.05% @ 103.28) pulled back after rising as high as 103.90 in what could be the test of the upper bound of a channel. It is trading above both the 50 and 200 MA and both RSI and MACD are positive and upward sloping.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Click HERE to READ more Market news.

Marco Turatti

Market Analyst

HFMarkets

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.