The Australian dollar has taken a beating in recent trading days, as the selling in it was mainly a result of the recent NZ election which dragged on the AUDUSD. This may come as a surprise, but there is some correlation between the two when it comes to their pairing with the USD. However, this selling has now stopped and markets are focused on the CPI data due out in coming days, which will provide some strong direction. The current expectation is a big rise in CPI data from 0.2% q/q to 0.8% q/q, which would bring inflation in that 2% target. Going further above the 2% target we can expect this to raise the attention of fixed rate markets who will be looking to see if this gives ammunition to the Reserve Bank of Australia to lift rates. The economy does seem to be bouncing back so this catalyst could lead to the bulls rushing back into the AUDUSD, as it continues to look stable and lack any political risk when compared to NZ at present - which has a degree.

With all this in mind where to for the AUDUSD. Well there are two ways to look at it and a weaker USD is not the answer here. If we do see a weaker CPI result then I could see the AUDUSD whacked and pushed lower to support at 0.7729, but it shouldn't have a massive impact. On the upside if we saw a CPI reading that beat expectations and markets felt it might be sustained then I could see resistance at 07900 targeted, with long term upside potential of hitting further resistance levels at 0.8000. Either way you look at it there is potential for bigger movements in the AUDUSD and potentially the AUDNZD as well, but CPI figures will have a big impact on market sentiment for the rest of the week.

Shinzo Abe got what he wanted as he swept back into power after this weekend's elections and the USDJPY was quick to respond by losing some ground on the Monday open, as Yen bulls appeared in the market. The continuation of Abenomics will be interesting, it has been one of the greatest economic experiments of its time. The reality though is that it has not really caused the expected result and may have created more problems. Markets however are expecting that the Bank of Japan governor will be replaced and another more hawkish governor could be brought in to create further change from a monetary policy point of view.

For the USDJPY traders it's a good time to be bullish, but also realise that the USDJPY does like big levels and to move sideways from time to time as well. Resistance at 114.258 thus far has been a hard ask for the market and I am expecting to see a real test here. If we can see a push through then further extensions to 115.322 are likely to be on the cards here. But USD strength will also need to hold up and it has suffered recently.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

The Australian dollar was thumped by the market today as CPI data missed the mark coming in at 0.6% (0.8% exp) leaving the market with a bitter taste in its month. On the back of higher oil prices and retail prices many had expected to see inflation lift and even hit the magic 2% inflation figure which might prompt the Reserve Bank of Australia into action. Sadly, it was not meant to be and the weaker figure coupled with global sentiment of weaker inflation in the mid range term means it's unlikely the RBA will get to raise rates anytime soon. So where to for the AUD? Well with the US government pushing its tax reform this could certainly boost the possibility of increasing US GDP and the USD for the most part. There has been a lot of weakness for the USD recently and that has boosted things, but for the most part it does seem realistic that they might be able to get it through. This would obviously play out well for the AUDUSD bears, especially if we continue to see weaker data in the long run.

So far the AUDUSD bears have slashed down the charts at a blistering pace before hitting the 200 day moving average coupled with support around 0.7687 and pausing for a breather. Given the recent weakness in the commodity currencies I would not be surprised to see further falls down to the next level of support at 0.7624. Nevertheless, the AUDUSD does have a habit of bouncing back, so in the event it did I would expect the potential for it to modestly rise to 0.7748, but it would be hard pressed to get higher to resistance at 0.7821. In any case I do believe that the bears may hang around for some time yet and market traders are likely to target key support levels until they find any hope for the AUD.

The UK has always been struggling with the recent Brexit negotiations but thus far FTSE 100 traders have managed to avoid the brunt of it. Not to so much today as global equity markets took a big tumble, despite growth forecasts being upgraded in the US. Markets at the moment seem quite skitterish and we are starting to see long candles, which means traders are getting very aggressive to defend these bullish positions at times.

The FTSE 100 is a fantastic case of this as we saw an aggressive dive today, followed up by some aggressive buying shortly after to bring it back into line. Support was touched at 7436, but traders were quick to defend this level, but the bears still took considerable ground. The 200 day is moving up the chart and if we break through support at 7436 then I would expect an extension further down to this level. Resistance levels can still be found at 7551 and 7600, with the potential to breakthrough looking very remote at present.

Currencies stay range bound ahead of Fed’s decision

It is a quiet Wednesday in the currency markets. Traders are favoring to remain on the sidelines ahead of multiple key risk events, including the Federal Reserve monetary policy decision later today; the Bank of England’s rate decision on Thursday; President Trump’s nomination of the next Fed Chair; the U.S. tax reform announcement and Friday’s NFP report.

Today’s FOMC meeting will not be accompanied by an update on economic projections, nor by a press conference. Traders have to act on very few amendments on a 500 words statement. The main theme is unlikely to change, and the Fed will stick to its plans of gradual tightening. However, recent economic releases have shown significant improvement in the U.S. economic activity, and GDP has grown 3% for two consecutive quarters, suggesting that we may see slight, positive changes in assessing economic activity.

Despite an uptick in headline inflation in September, core CPI continued to miss estimates, and remained below the targeted 2%. Thus, I expect little to no change on inflation assessment.

Overall, the Fed will likely meet market expectations, by keeping interest rates unchanged in November, and signal a rate hike in its final meeting in December.

President Trump’s nomination for Fed Chair on Thursday could easily overshadow today’s statement, especially if Fed Governor Jerome Powell is not his first choice. Powell has been supportive of Janet Yellen's policy of gradual tightening in monetary policy; thus, I do not expect big moves in Treasuries, or the U.S. dollar, if he is nominated. However, if Stanford University’s Professor of Economics, John Taylor, is nominated instead, expect big moves in Treasury yields and the dollar, which could appreciate sharply against its peers. According to Taylor rule, a forecasting model that determines where interest rates should be, based on targeted inflation and full employment, interest rates should be much higher the current levels.

The Kiwi was the only outperforming currency today, surging 1% against the dollar after labor market statistics showed that the cost of labor grew 1.9%, and the unemployment rate fell to a nine-year low. If wages continue to show signs of strengthening, the Reserve Bank of New Zealand will likely start raising rates next year, as opposed to earlier forecasts of tightening in 2019.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

The build up has begun for tomorrows NFP announcement and the market is betting big time on a strong result of 313K; this is a very large expectation, but it makes a lot of sense when you consider the seasonal impact that Christmas has on markets. Labour markets certainly boom during this period and even part time workers are considered part of the work force. I will say one thing, with such a large number it will be hard to beat, and I'm not certain that markets will take kindly to anything below the 313K, so it could be the NFP of the year on this basis. Markets will also be digesting the recent announcement that Powell will take over from Yellen as the FED chair. The markets thus far have been positive regarding this, with a number of heavy weight finance figures speaking out in favour of him. Many had expected a hawk, but the reality is that he's likely to take over from the Yellen framework and continue it in the short to medium term until he has a good grasp of the situation.

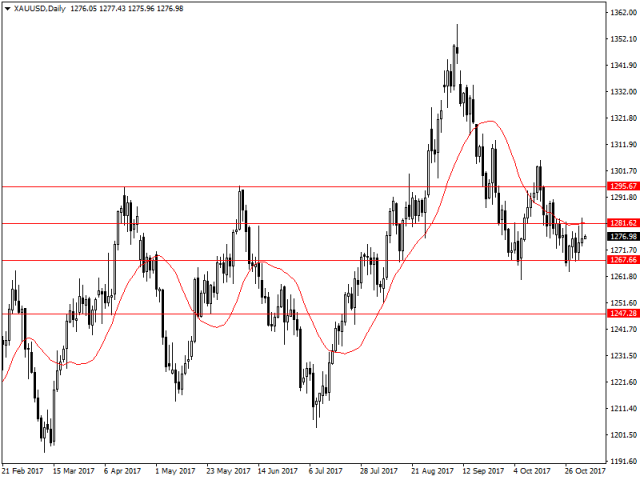

For the NFP traders, the metal markets is always the big calling when it comes to movements. Gold has thus far been creeping up on whatever USD weakness it can find, which is not surprising as the bulls are always there. Any NFP weakness tomorrow could see gold catapulted above the current resistance level at 1281 with the potential to even break through 1295 if it's quite bad. In the event it's a very strong result and in line with expectations then 1267 and 1247 are likely to be key levels of support for the gold market. All the moving averages at present are not likely to impact any shifts upwards or downwards so it will be a case of playing of key price levels that the market can digest at this present time.

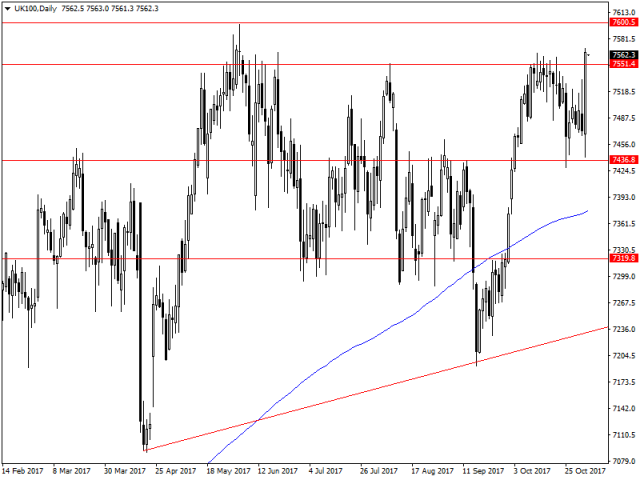

It was also a big day for the British market as the Bank of England raised interest rates by 25 basis points, leaving the intraday banking rate at 0.5%. This move had been widely expected, but the comments afterwards helped drive the pound down and encourage the doves in the market as the Bank expected inflation to taper off (as the pound stabilised) and also Brexit would bring uncertainty to the market causing issues in the long run.

The big benefactor of this was of course the FTSE 100 which lifted sharply on the news as the bulls rushed in to take advantage, and as the UK oil producers showed strong earnings as well. The market is now poised to have another crack at resistance at 7600 and NFP could be a catalyst which could push it through tomorrow as well. In the event that markets fall back down support at 7551 and 7436 is likely to be key levels, and markets will be looking to stop the rot if anything does transpire.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

The New Zealand government continues to be in the eye of traders as the current changes to the Reserve Bank of New Zealand look to be fast tracked. So far what we know is that the focus will not only be on inflation, but almost full employment for the NZ economy. This should come as no surprise given the recent elections and the want for the government to change to focus on this. Additionally, there is the need for a change on current FX policy which could have far reaching impacts on the NZ economy, as the current minor party (NZ first) wants to see the RBNZ intervene in FX markets to help drive export markets and keep the NZD lower. This has been seen as futile in the past given the RBNZ being quite small compared to world markets, so it could cause minor issues going forward. Either way markets are not currently upbeat regarding the prospects of the NZDUSD, but I believe the NZD is starting to stabilise compared to other currencies and is showing the odd signs of the bulls back in the market.

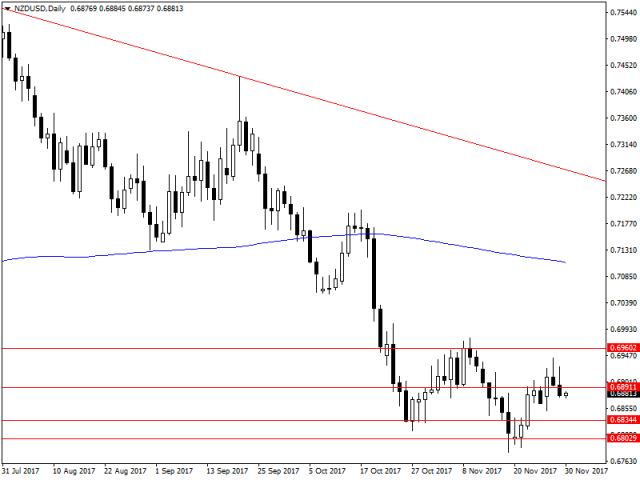

So far the NZDUSD bull have managed to claw back a considerable amount of ground in the face of uncertainty in the NZ economy. For me resistance at 0.6960 is the current strong level that is holding back any further gains on the charts, the reason being is that no one knows the current direction of the NZ market after elections. If it was positive then I would expect a jump to 0.7029, but a potential slow down shortly after this jump. In the event we did see minor falls on the charts then support could be found at 0.6891 and 0.6834 respectively, with the ability to go lower as markets are considerably more bearish after the recent election.

Oil has been one of the big jumpers on the charts as markets have been quick to worry about the situation in Saudi Arabia recently. The anti corruption crackdown has taken a few high profile heads, and the markets are worried about the state of play from the world's largest oil producer. Certainly, there have been drawdown's on global oil supplies, but the shakeup of affairs could have the largest impact in the long run and drive oil prices higher in the short term.

So far Oil bulls have charged forward and knocked out support at 56.17 as the oil markets continued to run higher. Resistance level can be found at 59.08 and 62.12 on the charts with the potential to go higher if more political uncertainty presents itself. There is also the potential for charts to dip lower and support can be found at 56.17 and 50.21 as the market looks to drift lower as news looks more promising potentially.

The Euro has been a star over the previous months, but it's becoming more and more lacklustre as the ongoing Spanish drama is still a thorn in the side of the Euro-zone. While investors love a bit of volatility, the Euro-zone seems to keep battling crisis after crisis trying to hold everything together as more moles pop every month to be whacked. Is there cause for concern? Well markets seem to think so as of late, and event EU retail sales figures y/y jumping to 3.7% (2.8% exp) were not enough to fight of the bears. Additionally, the US saw a strong JOLTS job openings figure of 6.09M (6.08M) which shows that the labour market in the US continues to not be at capacity. This can also be seen in the fact that wages have not grown as fast as economists had expected, which points to slack in the labour market that can still be filled. It would seem though that we are close capacity in the next year or two in the US if there are no negative economic events.

So for the Euro bulls it's been a tough ride over the past few weeks and the head and shoulders pattern that did occur is likely to keep going with bears taking full advantage. Target support levels for the market will be found around 1.1519 and 1.1433, with the potential for further lows if we see any further weak news on Catalonia. If we do see the bulls come back into the market I would expect to see resistance be strong around 1.1621 and 1.1719 on the charts. Additionally, the 20 day and 50 day moving average should be watched as dynamic resistance levels which daily traders have been respecting as of late. However, for the most part there is a clear trend of bearish sentiment which has the potential to continue for some time.

NZ dollar traders also went short today as the Global Dairy Index came in at -3.5%, obviously this is quite big news for traders as the Dairy industry accounts for 7% of New Zealand's GDP. But further to this we have the RBNZ rate statement due out tomorrow, and many are expecting some fireworks here. Not in the sense of a rate rise, but in the sense that change is in the wind with the new government wanting it to have stronger mandates. It will be a case of wait and see, and the prospect of a new governor is on the cards as well with the new left wing government.

For the NZDUSD traders there has been a failure to breach anything above the 70 cent market, which continues to act as a psychological barrier at present. Markets thus far are looking bearish and swinging lower just coming up short of support at 0.6891. There is further potential for moves lower to 0.6834 and 0.6802 on the charts. I would be surprised to see it spring back up higher, but if it does the 70 cent mark is likely to be a hard stop for the pair.

Sterling slides, Bitcoin tumbles & Investors seeking more clarity on tax reforms

Sterling fell more than 0.5% early Monday, after the Sunday Times reported yesterday that 40 Conservative Party MP’s agreed to sign a letter of no confidence in the Prime Minister, Theresa May. While this remains short of the 48 votes needed to force a new leadership, it still creates much frustration amongst investors seeking clarity on Brexit negotiations. With May’s position being potentially at risk and no significant progress after six rounds of talks with EU, Sterling may come under increased pressure in the next couple of days, with the 1.3024 support level at risk of being breached. A leaked letter from Boris Johnson and Michael Gove pushing for Hard Brexit, add to the uncertainty as House of Commons meet on Tuesday.

It is also a busy week on the UK’s economic data front, with Consumer Price Index, Producer Price Index, labour data and retails sales due to release. However, politics are likely to remain the dominant factor moving the pound this week.

For investors finding the low volatility environment boring, have a look at Bitcoin. The cryptocurrency lost more than quarter of its value after reaching a high of $7,888 on Nov 8. The cancellation of a plan to increase the bitcoin’s block size “Segwit2x” on Wednesday, is what to be blamed for the price crash, but given that prices rallied $400 on Monday it seems the news has been digested. We have seen similar steep falls in Bitcoin throughout the year; specifically in June and September, but every time a considerable decline occurs, new investors jump in to experience the new asset class. The increasing investor interest in the cryptocurrency market has pushed CME Group to announce the launch of a bitcoin derivative soon, indicating that more fund managers and professional investors will become involved. Although Bitcoin might not be a suitable asset for conservative investors due to its volatility, I still see a great potential ahead.

Given that the earnings season has come to an end, equity investors will shift their attention to the U.S. tax reform plans. There is a considerable difference between the Senate and the House on how to proceed, and if no clear path evolves, I expect a further pullback in equities. The Senate’s proposed delay of the tax cut until 2019 is definitely not what President Trump is looking for, so it remains to be seen whether he can push Republicans to unify when he returns from his Asia tour.

It should be all good news for global equity markets at present as the global recovery continues to tick along nicely. So far profits are up and the market has been bullish, especially around developed labour markets. However, have we overextended at present? If you've been watching some of the major indexes you might very well think that. Recent trends in global markets have so far been bearish which is a surprise, but when you consider the level of uncertainty and the fact that rates are on the move higher it does make for some interesting thoughts and trading ideas. So far yields are looking like they're increasing in the long run, which bodes well for investors looking to move out of equities.

The S&P 500 has come up short of the magical 2600 mark at present, this despite the recent news off the wire about NAFTA renegotiations being positive. PPI was also positive today, but once again markets were not having a bar of it, and looked to sell off. So far the S&P 500 has held up on support around 2580 where it has managed to sit above over the last few days, the 20 day moving average is also providing some additional support. Further movements lower are likely to hit key levels of support at 2565 and 2545. Just looking at the daily movements, it's very hard to say if this is the time for a correction. Certainly, markets are feeling like one is overdue, and historically data says that is the case. The question here is when and how bad, but for now the bulls have the trend and market corrections are rare for the S&P 500.

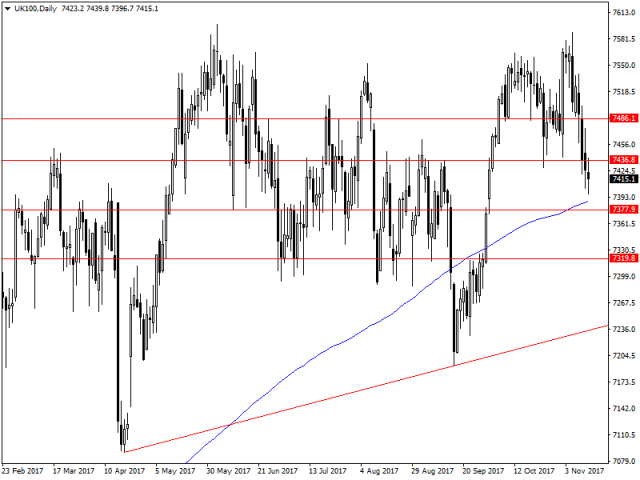

A quick glance across the Atlantic at the UK equity market and it's a similar story, just this time the market is being dominated by politics and of course the Brexit debacle. Mark Carney must have been breathing a sigh of relief today as CPI was not as strong as the previous month at 3% y/y, thus taking the pressure of the needs for any further rate rises at this time. Markets, however, were not so interested as the FTSE 100 dropped on the news and continued to be weighed down by global sentiment around equity markets.

FTSE 100 traders will be looking to extend the trend lower if with the bears, but so far we've seen weaker and weaker candles which is a sign of caution from them. There is the possibility of the bulls swinging back into the market here and potentially pushing for resistance at 7436 and 7486 on the charts. If the bears do extend lower than the 200 day moving average, it will be key to watch here to see if traders respect it. With weaker candles that could be very much the case. Support levels below this can be found at 7377 and 7319 for the bears.

It's been a positive day for US economic data as retail sales surprised analysts lifting to 0.2% (0.0% exp). This shows a strong build up in the period before Christmas where retail sales is generally quite strong as well, and will bode well for the economy and the FED which is a big follower of the consumption based economy that is the USA. Further adding to fuel to the fire was of course CPI data which I touched on yesterday with Core CPI y/y coming in at 1.8% (1.7%) exp. While not the magic 2% mark the FED does chase it was certainly a positive reading and shows that the economy is turning over nicely in America. The real question will now be if fiscal policy from the Trump administration and can translate into real gains for the economy, or if his legislation will continue to struggle through the house and senate in America. It would be a strong mover of the dollar is something was passed with tangible gains in the near future, but so far the market is in wait and see mode on the fiscal front.

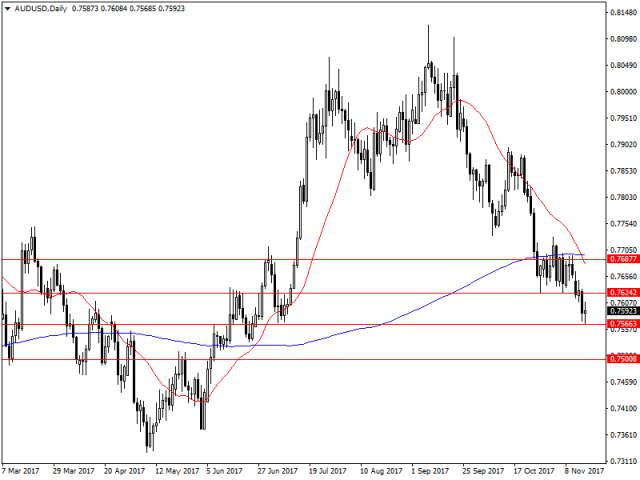

One of the major losers as a result of the USD boost was of course the Australian dollar which has lost ground after last night's economic data which showed wage growth being underwhelming. With the wage index coming in at 2% y/y (2.2% exp), showcasing that while the job market is strong wage growth is not following it and inflation will cause issues in the long run for the Australian economy if wage growth does not catch up. With the AUD now pushed against a wall traders have been of course waiting on the employment figures due out. Of course they've not been the best with employment dropping sharply to a reading of 3.7k+ (18.8k+ exp), but the unemployment rate falling to 5.4% accordingly adding some consolation for AUD bulls at present.

On the charts the AUDUSD has not been this low since July and markets will be looking to see support at 0.7566 on the charts or if it will struggle to extend any lower and we see the predictable bounce in the AUDUSD. As the employment data is bad markets have overreacted and driven the AUD lower to support at 0.7566 where it has looked to take a breather at this key level. If the bulls do come back into the market - and it's really a maybe - then resistance levels can be found at 0.7624 and 0.7687 with the respective movements if things became worse from a fiscal point of view. Reality is however, that the bears are likely to have another crack and potentially force it down to the 0.7500 key level at present with the potential to fall further at this present time.

The Tax bill has been talked about for some time, and today was the day for it. Obviously, it cleared the US house easily enough and is now on its way to the senate; where the republicans have control as well. What does this mean for markets? Well put simply it cuts corporation tax from the current 35% to 20% - a very large jump - which means US companies are likely to record larger profits which of course will have a flow on effect for the economy. The real question here is if the republicans in the senate will be able to push it straight through or will look to make amendments. They are after all different creatures in the senate and the tend to be more heavy handed when it comes to clearing large bills like this through government. However, with a two seat advantage it looks like it may just shine through and Trump will be able to sign it all off before Christmas - giving him his first major win of his presidency.

For equity markets the rally has been pretty sharp as a result of the tax bill. Traders are betting that in the long run this tax bill will unleash the corporate machine that is America and record profits will accordingly flow through. The S&P 500 today was a prime candidate for this as a I previously noted, and accordingly has rallied sharply. Resistance at 2580 was no match for traders looking to enjoy the rally today and now it's a case of targeting 2600 for many bulls in the market. If the senate does indeed push the bill through then 2600 may be a support level as the market will jump sharply I feel - given it's the last hurdle. With a tax reform like this the possibility of even pushing the 3000 mark becomes all the more realistic. If we see the bill struggle then we could see sharp drops on the charts to support levels at 2565 and 2545, with the potential to go further as it feels a lot is riding on this bill in the equity markets.

The Australian dollar was one I also touched on yesterday and while the unemployment rate fell to 5.4% (5.5% exp) the participation rate was lower, and accordingly the creation of new jobs only came in at 3K so it was disappointing for traders in reality. I still feel that the AUD will struggle in the long run given the pressure on the economy, and as the USD continues to find favour with traders again.

The AUDUSD on the charts currently has been trading between resistance at 0.7462 and support at 0.7566, with market expectations of potential falls lower. The 0.7500 psychological level is currently likely to be the largest target if the trend continues. However, we could see a bounce here and a retest of resistance levels at 0.7624 and 0.7687 on the charts.

The Euro had a pause for concern in the evening trading session as the coalition talks in Germany fell apart leading to a political crisis in Germany. This now presents the toughest challenge Angela Merkel has felt in over 12 years of being at the top, however, she seems somewhat composed and is keen to send the parties back to the polls in order to get a majority government. So far though polls have predicted that anti immigrant parties are likely to gain more momentum than the traditional centrist parties which have dominated German politics in recent decades. And for Brexit this will certainly put pressure on the British government now that Merkel is currently off dealing with her political crisis, rather than being focused on there's. For some time many had expected her to get involved and sort out the crisis, but that's certainly not going to be the case and £40 billion bill the UK is offering to settle the bill is being put to the table.

The British governments ability to settle the bills is likely to be a game of brinkmanship and the EU does not have to blink at all. What could well be worth their time is to let it play out internally as right now a number of backbencher Tories are upset over the size of the number and could in theory force a leadership vote. While plausible I do believe that the government is likely to try and push it all through as rapidly as possible in order to get backing from business. Either way the pound is likely to encounter some rough waters over the course of this week as a result.

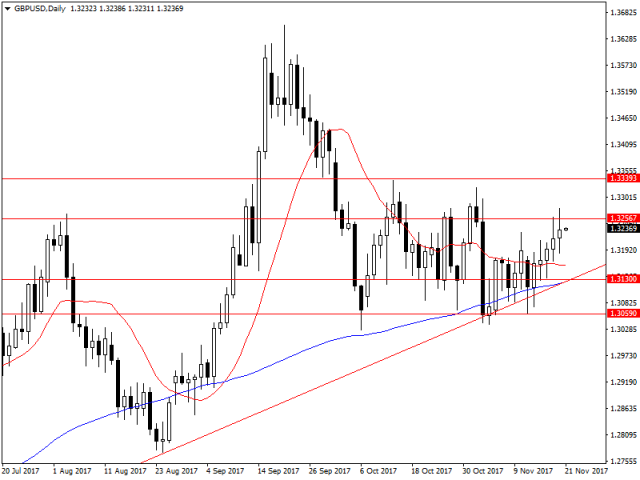

On the charts the GBPUSD continues to be inching its way higher on the charts, and thus far it's been on the back of some USD weakness which has been apparent. However, the recent moves higher have shown an abrupt weakness in bullish potential and we could see bears come back into the market to tighten things up before breaking out. Resistance levels for the GBPUSD can be found at 1.3256 and 1.3339, but the band in between this is likely to see a lot of action. In the event that markets turned south they would have a tough time battling the 100 day moving average which has been acting as dynamic support, and also support levels at 1.3130 and 1.3059. A breakthrough of these support levels could send the pound tumbling though.

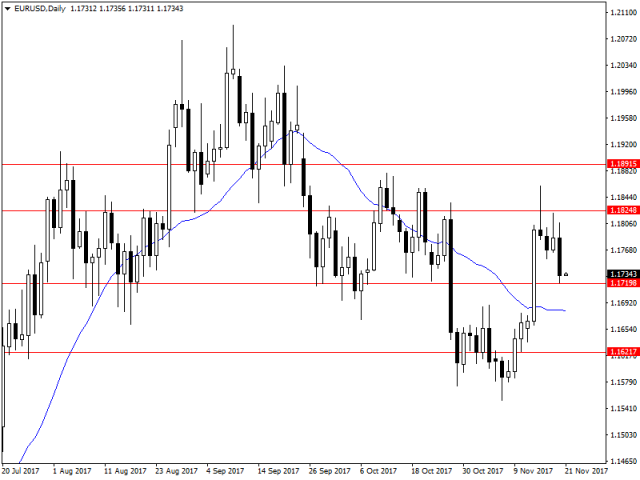

The EURUSD is also looking weaker after the political news out today, and for me the focus will be playing of the political news out of Germany going forward. Key resistance levels can be found at 1.1824 and 1.1891. Support levels can also be found at 1.1719 and 1.1621, with the trend looking all the more bearish as of late. Certainly also for the euro the USD weakness will be a primary factor, but so far it' s a mixed bag.

Global stocks rally, Sterling on standby ahead of UK budget

The healthy combination of rising corporate profits, strong global growth and cautious optimism over U.S. corporate tax cuts, simply reinvigorated global equity bulls on Tuesday – boosting stocks across the globe.

Asian shares headed for a record close during early trading on Wednesday, following Wall Street’s robust gains overnight. European markets concluded mostly higher on Tuesday and may open on a positive note today as market players continue to shrug off the political uncertainty in Europe. With U.S. stock indexes marching to record highs yesterday as technology and health stocks rallied, it will be interesting to see if the upside momentum is maintained this afternoon.

Chancellor Philip Hammond in the spotlight

Chancellor Philip Hammond will be in the limelight today as he presents the U.K. budget statement to the House of Commons. While Hammond’s speech may revolve around managing the housing crisis, investors will be paying attention to the Office for Budget Responsibility (OBR) which is expected to trim Britain’s GDP growth forecasts. If the overall tone of the budget statement is gloomy and Brexit concerns making an appearance, Sterling is likely to find itself under renewed selling pressure.

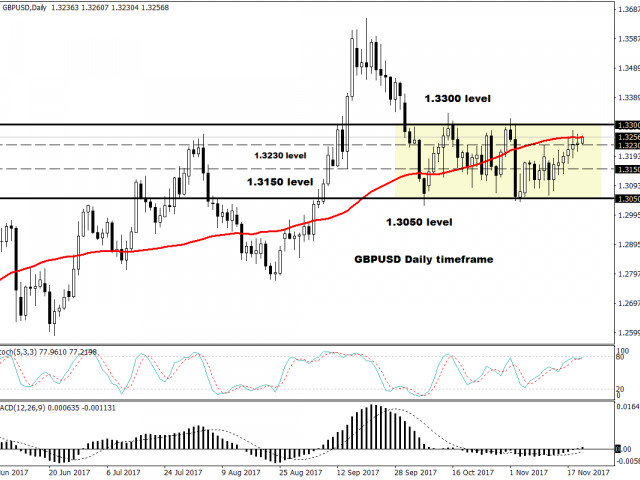

Taking a look at the technical outlook, the GBPUSD has found light support at 1.3230. An intraday breakout above 1.3250 could encourage a further incline towards 1.3300. Alternatively, a failure for prices to keep above 1.3230 may encourage a decline to 1.3150.

Dollar lower ahead of FOMC minutes

The Greenback weakened against a basket of currencies on Tuesday, after Yellen’s cautious remarks reinforced market expectations of the Federal Reserve raising interest rates at a gradual pace.

Yellen cautioned that raising interest rates too quickly could obstruct the Feds efforts to reach the golden 2% target and reiterated the fact that this year’s low U.S. inflation remained a mystery. With the outgoing Fed chair uncertain over the stubbornly low inflation being transitory, investors were left pondering over how this could influence the central bank’s monetary policy strategy in 2018.

Much attention will be directed towards the minutes from the latest FOMC meeting this evening which should offer further clues on the central bank’s outlook future interest rate increases. With markets widely expecting U.S. interest rates to be increased in December, investors are likely to closely scrutinize the minutes for fresh insight into monetary policy beyond 2017.

The Dollar could receive a boost if the minutes are presented with a hawkish touch, alternatively, if the minutes express concerns over low inflation and fail to bring anything new to the table, sellers may make a move. From a technical standpoint, the Dollar Index is coming under pressure on the daily charts with resistance found at 94.00. Sustained weakness below this level may encourage a further decline towards 93.50. Alternatively, a breach back above 94.15 puts this current bearish setup at risk, with the next level of interest at 94.50.

FOMC meeting minutes are always greeted warmly by the markets, as a glimpse of the potential future direction of the FED going forward, and today didn't disappoint at all. As predicted the FED was positive about the possibility of a December rate hike before the year goes out, and the market has aptly priced this in. Markets on the other hand were caught off by certain members reluctance to actually lift rates as they felt inflation was starting to slow down and the previous large rises may not continue going forward. Now with Yellen set to resign and the new head of the FED taking over, it may be the case that we do see more hawkish movements. But the board is a democratic vote, so unless we see real movement there it becomes very unlikely at this stage and the doves could be staying on for some time.

For traders the USD sell off in safe-haven currencies was strong with the USD losing a number of points especially against the Yen. USDJPY was by far the most volatile trade of today, which surprised many given how flat it had recently been, but markets were quick to punish the FED over its dovish comments. One of the major reasons behind the sudden appreciation of the Yen is that thus far Abenomics has not been as active as expected and it continues to be at a risk of being devalued quickly. It's also a fantastic storage for traders looking for some sort of safety within the markets and a traditional one at that as well. However, for the USDJPY bears the time to jump was today and they certainly did.

USDJPY bears crashed through the 200 day moving average ruthlessly as they looked to push the pairs to strong support levels. Support at 111.133 was able to holt the downward trend, but so far is the only thing holding back the USDJPY from storming any lower. Markets looking to swing lower further are likely to find another strong level of support at 110.202, but the market may take some breather here and give up some gains. For traders looking for a bounce higher then resistance can be found at 111.944 and 112.787. The reality for the bulls jumping back in though is slim, as this bearish trend is likely to push traders back in the water in search of blood.

After the recent failures of traders to break through resistance at 114.359 over the previous month, it's no surprise that the market has jumped on a bearish trend. The question is though will it continue to run, or will markets look to pause and take stock of the volatility we've seen today. My thoughts are that it could potentially slow down but still trend, which would be promising for traders looking for an easy wave.

Stocks drop, currencies range bound & bitcoin eyes $10,000

Most Asian indices edged lower on Tuesday, following a mixed session on Wall Street yesterday. China is becoming a key market to watch, as it’s leading the direction for other markets across Asia. Rising bond yields are threatening corporate profit margins for the second largest economy; meanwhile Chinese authorities are helping to drag equities lower, after sending alarming messages about a potential bubble being created in large-cap firms. Given that China continues to focus on quality rather than quantity growth, it’s not surprising to witness action of this nature from the Chinese government in an attempt to mitigate bubbles in asset prices. However, such actions may have a negative impact on sentiments that could spread across other Asian markets.

U.S. equity traders are in a wait-and-see mode. President Trump will meet senators today at their weekly policy lunch, to ensure that Republicans are on the same page regarding the tax system overhaul. I firmly believe that U.S. legislative tax reforms are strongly “priced in” the U.S. markets, thus if significant tax reforms do not pass, I expect a substantial decline in major indices, particularly in small caps. Given that the effective tax rate currently stands at around 27%, taxes should be brought below 25% to be effective. Republican Senator Ron Johnson said he would vote against the bill unless his concerns about the legislation are resolved. Given that other Republican Senators share Johnson worries on deficit implications, passing the bill does not seem to be a done deal yet.

Currency markets were trading in narrow ranges early Tuesday, as investors brace for UK bank stress test results, BoE’s Carney Speech and the Fed speech, including Powell’s Congressional address. On the data front, the U.S. Goods Trade Balance, and the Housing Price Index are likely to have minimal impact on the USD.

At the time of writing, Bitcoin scored a new record high of $9,886 in an attempt to break above the critical $10,000 threshold. Bitcoin has become a very hot topic and many fund managers have raised the price target for the cryptocurrency. Yesterday, former Fortress hedge fund manager Michael Novogratz commented on CNBC, that bitcoin could be at $40,000 by the end of 2018 and he expects that total market capitalization could reach $2 trillion, from $309 billion currently. I think that we will hear more skyrocket predictions, but few will provide an economic metric that supports their valuations. It will be interesting to see how the market reacts when Bitcoin breaks above $10,000.

It's been a crazy day on the markets and the GBPUSD has been a clear winner when it comes to movements today as the Market has reacted positively to the so called 'Divorce Bill' from the EU that Britain is meant to pay. So far people are expectong the figure to come in around 50-60 billion pounds that would be paid out over 40 years. Obviously, this is a large number for any sovereign nation, but it enables Britain to plow forth in its so called negotiations. The market is now looking for the next steps for the UK economy, as it expect to see some sort of trade negotiations come out of all of this. I do think that it might be a bit of a while off that we do see something realistic, the fact being that a) the UK has no strong leg to stand on, and b) it's always a long road to what people expect will be a result. Either way the volatility in the GBPUSD is likely to continue into the near future especially with the current pace of news and politics involved in Brexit.

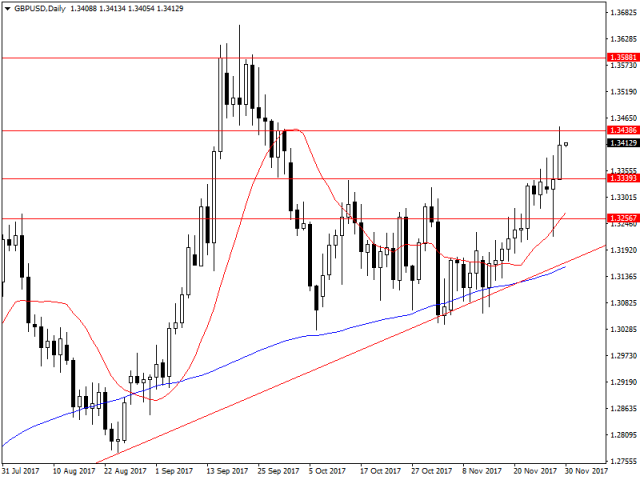

On the charts it's clear to see that the bulls are back into the market and are climbing higher. Yesterday we were talking about the 1.33 levels, and today we are in the 1.34 levels which shows the market is keen on these talks. After touching resistance at 1.3438 the market has pulled back to take a breather, but the real key level is to be found at 1.3588 which is where bullish traders will be looking to aim in this market. In the even the bears do regain control and look to push it lower then support at 1.3339 is likely to be a prime candidate for support as well as 1.3256. Traders should also be aware of the previous trend line which continues to be an obstacle for any bears in the current market.

The US also continued its stellar run today with US pending home sales m/m lifting by 3.5% (1% exp) once again showcasing the strength in the USD. On top of the traders were also somewhat bullish about the first round of the senate tax review of the Trump tax bill, which is likely to boost the US economy - even though running a deficit for a bit. One of the big losers for this has been the commodity currencies which have been bearish against the USD with all this support.

For me the NZDUSD continues to be one of those currencies that will struggle with a resurgent USD in the current market climate. So far all the candles have shown exhaustion by bulls in the market as the NZDUSD dipped under resistance at 0.6891. The market is now looking to extend further lower to 0.6834 and 0.6802 on the charts, as the market looks to push it back into the red. For me the bulls are going to be a real threat until the USD gives up some ground as the NZ economy is still struggling in the interim while it figures out a new government.

The Canadian dollar was back in focus today as the market was looking for hawkish signs from the Bank of Canada, on the back of the recent interest rate statement. The interest rate was kept at 1% however, and the market was caught off guard by the dovish comments made by the BoC. While the economy has been adding new jobs and Fridays figures were a testament to that (+441,400), the BoC is still concerned about the NAFTA negotiations that are ongoing, as well as recent housing market developments. This came as a shock for a lot of market pundits, but more important it forced forecasts further out for future rate rises, while before the market was betting heavily on the BoC to come through and cause further positive betting on rate rises.

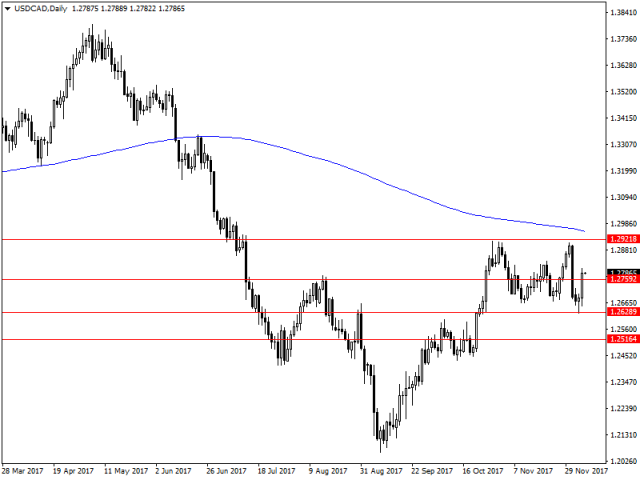

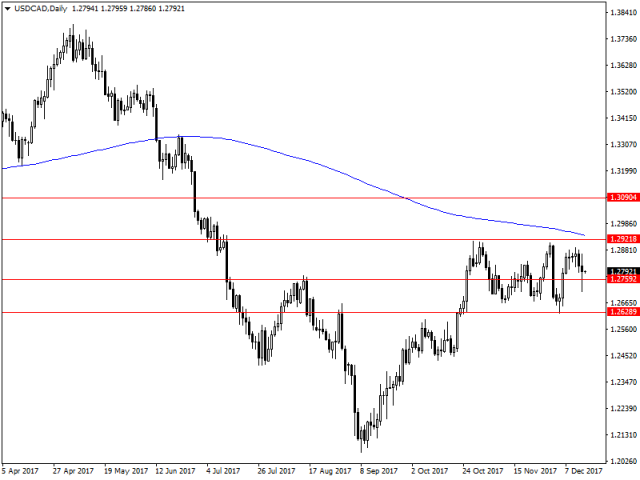

The USDCAD was quick to jump on the back of the news out from the BoC, as USD bulls rushed away with all the recent gains and pushed through resistance at 1.2759. Further levels higher can be found at 1.2921 with the potential for any higher gains to the 200 day moving average - which would be very hard to push through. If the market does turn around and head back south then support at 1.2628 and 1.2516 are likely to be the prime candidates for bearish traders, with the area between these two levels likely to act as a key selling point on the market.

Crude has been one of those funny players in the market as of late with a bullish rise, which has been purely on the back of OPEC extending production cuts. Now for many this comes as no surprise as the oil market did need to stabilise but today's fall caught many off guard given that the drawdown came in stronger than expected at -5.61M (-2.5M exp). The reason for this was refined oil products with gasoline showing an increase to 6.8M barrels, beating market expectations and causing the oil market to sell-off. Selling pressure is common when you have a build up of refined products as the market might start to think it's flagging or peaked already.

Oil now finds itself in a weird place at present as the recent rise has struck strong resistance at 59.08 in this market, and the fall today hit the current old trend line which the market is respecting before taking a pause and stopping all together. I'm not sure if there is further potential falls on the cards given the bulls have been so strong, and this could be an excuse to unwind. However, if the trend line did break then support could be found at 55.14. If oil does indeed jump back higher, then for me resistance at 57.38 and 59.08 are the key levels traders will look to target. Expectations are though that 59.08 will be the level to beat currently.

Bitcoin future trading kicks off; Investors awaiting central banks decisions

Trading bitcoins entered a new phase today, after Chicago’s CBOE listed the first futures contract on the cryptocurrency. The initial reaction was beyond expectations with the futures contract climbing more than 20% and triggering two trading halts. CBOE’s website experienced unprecedented traffic which may well have sent a new benchmark, the frenetic activity lead to delays and outages. So far, it seems professional investors aren’t willing to bet against the bitcoin, despite the many warnings of a bubble that will burst soon. Many traders aren’t even interested in the price direction, but the listing of the futures contract on CBOE and later next week on the CME, will provide them an arbitrage trading opportunity due to the vast pricing differences. However, the arbitrage trading will lead to improved price efficiency and probably less volatility. After volatility settles down, the focus will return to the price direction.

Central Banks Meetings

Currency markets were trading in tight ranges early Monday with the dollar slightly weaker against its major peers. Expectations of the Fed hiking rates on Wednesday, stands at 90.2% according to CME’s Fedwatch tool which means the disappointment in wage growth won’t shift the needle for US monetary policy. However, it isn’t the rate hike that will move the dollar on Wednesday, it’s the tone, economic projections and the dot plot. Given that we’re getting closer to a deal on tax reforms, the Fed might become slightly more hawkish. It remains to be seen whether this will shift up the Fed’s dots for future interest rate expectations.

The European Central Bank and Bank of England are also meeting this week. Despite no substantive monetary policy changes expected, the language might still move the Euro and the Pound.

Will the Fed support further rotation in stocks?

Tech shares have been in focus over the past two weeks after the S&P tech index plunged more than 4% between 29-Nov and 05-Dec, before recovering last week. The fall in Teck stocks wasn’t accompanied by a selloff in other sectors, particularly the financials which have been on the rise. This is a classic type of rotation with active managers balancing their portfolios before year end. Tax reforms don’t seem to be of great support to Tech firms, given that their effective tax rate is considered to be the lowest in the U.S. Meanwhile, it’s a big deal for the rest of the U.S, with financials having an effective tax rate of more than 30%. The new Fed Chair, Jerome Powell will likely speed up deregulation for the financial sector which will drive more inflows. And of course, higher interest rates for 2018 will further support the banks' profit margins. That’s why the trajectory of interest rates in 2018 will likely lead to more portfolio balancing before year end.

EU Summit

The breakthrough in Brexit talks on Friday was a great relief for policymakers, who can now move to phase-2 of the talks. Interestingly though, Sterling instead of rising sharply, dropped on the news. Investors seem reluctant to buy Sterling as they view the next phase more complicated than the first. They want to see details of the transition agreement and trade talks concluded before buying Sterling. I don’t think the EU summit on Friday will reveal much, but blessings from EU leaders might lend some support to the Pound.

It's been a funny day for the USD as it slipped lower on Tax legislation worries. For the most part it has fallen around two senators who are keen to fix the current child tax credits. In reality this is something republicans are likely to help remedy in order to get this bill over the final hurdles and in front of the president to sign before Christmas. However, for me the big mover - and what might have a much more interesting impact - was of course today's retail sales which lifted sharply to 0.8% m/m (0.3% exp). This is a very strong move just ahead of the December rush season and in return we could expect to see GDP forecasts raised for the 4th quarter going forward. I would be surprised if we didn't see solid earnings this season in the equity markets as well given the huge rises in consumer and business confidence. For now it would seem the Trump effect might be still there after all heading into the new year.

One of the key areas this was felt was on the USDCAD which was swinging heavily today, not only on the USD weakness but also Bank of Canada comments which pushed up the chances of a rate hike for March next year. For the most part the USDCAD has been ranging for some time, and it has struggled to break through the major resistance level at 1.2921, which has so far seemed like an impossibility at present. One of the main reasons also has been the 200 day moving average bearing down on that level which of course adds further pressure. At the same time the swing lower today failed to stay below support at 1.2759 which leads me to believe that the bulls are still in this market despite the Canadian recovery we've seen. If the bulls do leap back into the market 200 day moving average will be the key level to close above, and if we do close above then expectations are that we could see a move upwards to the 1.3000 level. For now though it's a case of waiting to see if the ranging does stop and the trends continue.

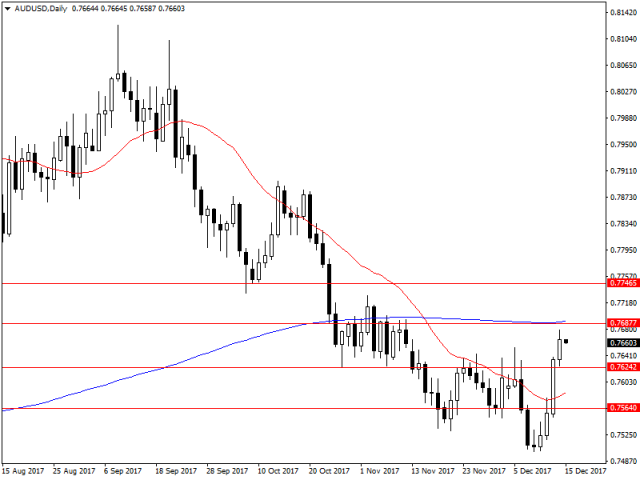

The other key one to watch out for is the AUD, with the market likely to be looking forward now to next week's RBA minutes on the economy and their thoughts after the most recent unemployment figures. We could certainly see the case made for a potential rate rise in the future, but for now it's a case of wait and see - even though the market is fairly bullish.

Chart wise, and it's clear the AUDUSD bulls are back in fashion and looking to make up some ground. After the positive news yesterday and weak USD it is a surprise to see that it has failed to climb higher to the 200 day moving average and resistance at 0.7687. I still believe this is a key level to watch and if we do see further extensions it could lead to bigger things. For now though like the USDCAD it's a case of wait and see as the market looks to enter Friday trading.

Daily Fundamental ForexTime ( FXTM ) Equities reaction muted on tax breakthrough; Watch the bond market

Asian markets woke up on Thursday to the news that Republicans had passed the long-awaited tax bill. President Trump is now just a pen stroke away from overhauling the tax code. Interestingly there aren’t any fireworks on the announcement of Trump’s Christmas gift; because as expected, the good news is already priced in.

In fact, the reaction was more evident in fixed income markets. U.S. 10-year bond yields traded above 2.5% for the first time since March 2017, allowing the yield curve to steepen after flattening for most of 2017. The spread between 2-year and 10-year treasury bonds climbed more than 12 basis points, reaching 63 basis points, after falling to its lowest level in a decade last week. The spike in long-term bond yields is supposed to be positive for the U.S. dollar, as it suggests the Federal Reserve should become more aggressive in tightening policy next year. However, the dollar’s reaction was muted because there’s another side to this story. The additional supply of U.S. bonds due to the unfunded tax cuts, will probably make U.S. treasuries less attractive in the longer run, and given that most central banks are trying to catch up with the Federal Reserve, yields in Europe and other markets are also anticipated to move higher in 2018, thus narrowing the interest rate differentials gap.

The enormous expected increase in U.S. deficit will also put the U.S. sovereign credit rating at risk. If any of the credit agencies- Standard & Poor’s, Moody’s or Fitch downgrades the U.S. sovereign rating, yields will spike even higher. However, the impact on the dollar won’t necessarily be positive, with the opposite reaction being more likely.

The Yen’s reaction was also muted to Bank of Japan’s monetary policy decision. As expected, the central bank kept interest rates unchanged at -0.1% and maintained its 10-year bonds yield target at around 0%. Given that weak inflation is expected to continue dominating the monetary policy outlook, I don’t expect any significant change in policy next year. Thus, the Japanese Yen will continue to take its cue from risk appetite/aversion in equity markets for the foreseeable future.

Euro traders are awaiting the outcome of today’s Catalonia’s election. Polls are suggesting that it will be a tight race between the Catalan Republican Left party, which supports independence and Ciudadanos which is in favor of a unified Spain. Given that the election is not expected to be decisive and parties may form coalitions to govern, the risk of tensions flaring with Madrid again, remain limited.

With only two trading sessions remaining for 2017, liquidity dried up across the global markets. This has been obvious in U.S. and European equities, where volumes dropped significantly. However, some investors continued to tweak their portfolios slightly, leading to insignificant price action. I don’t expect equities to deviate much throughout Thursday and Friday.

Interestingly though, traders continued selling off the U.S. dollar. One could blame Wednesday’s U.S. consumer confidence report which fell from a 17-year high, but the dollar was declining before the release. I think the best explanation for the dollar weakness is the sharp fall in U.S. Treasury yields.

10-year bond yields dropped 7 basis points on Wednesday, to reverse almost 50% of the gains from mid-December towards last week, where yields broke above 2.5% for the first time since March 2017.

Despite appetite for risk sending Asian equities to record highs on Thursday, the safe haven Yen is outperforming its major currency peers. USDJPY dipped below 113 for the first time in six trading days after the release of Bank of Japan meeting minutes. Some members are considering tightening monetary policy, if the economy continues to improve next year. This would be a significant shift in strategy for a Central Bank thought to be the last to exit the unconventional stimulus packages. However, I don’t think the BoJ will move anytime soon due to subdued inflation; but, given the lack of liquidity, moves in currency markets may be exaggerated.

Commodity currencies are also enjoying a decent upside, after copper prices rallied to their highest level in almost four years.Oil prices remained close to a two and a half year high, and gold hit a one- month high. Considering that no Tier One economic reports will be released, the Aussie, Kiwi, and Loonie will continue to follow commodity prices direction.