IFCMarkets

Broker Representative

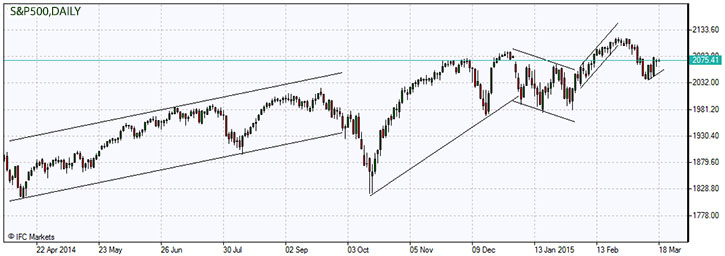

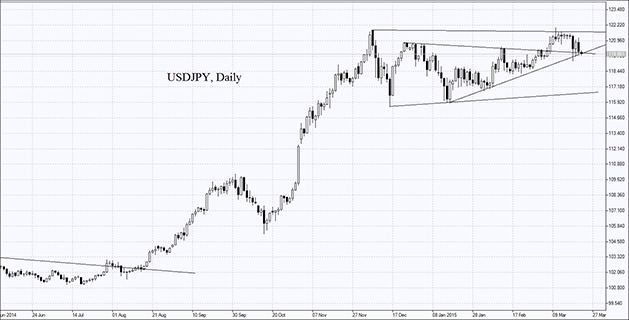

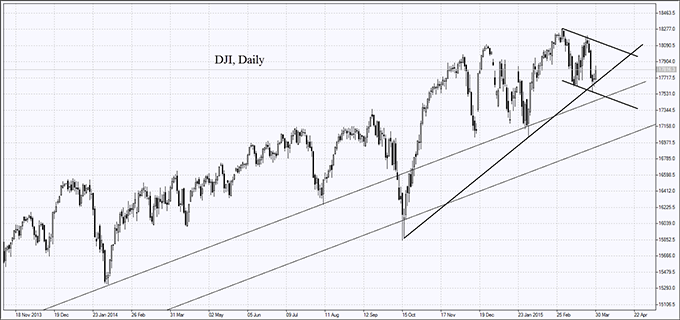

US stocks retreated on Tuesday from record highs. Nasdaq pulled back from the psychologically significant 5000 level. The investor sentiment was dampened by lower-than-expected growth in monthly car sales. US sales of cars and light trucks slowed to a ten-month low in February, registering at an annual rate of 16.23 million. Ford and Fiat Chrysler shares declined sharply. Ford Motor Co fell 3.3% after the company reported that its February US vehicle sales fell 1.9% from a year ago. The dollar inched lower against key rivals after strong economic data from Europe indicated that European economies are on the path of recovery. The ICE US Dollar Index, a measure of the dollar’s strength against six of its major trading partners, was down 0.06% on the day to 95.4090. Today at 14:15 CET February ADP Employment Change will be released in US. The tentative outlook is positive for the dollar. At 15:45 CET final Services PMI for February will be released by Markit, and at 16:00 CET the February ISM Non-Manufacturing PMI will be released. The tentative outlook is positive for the dollar. At 20:00 CET the Beige Book will be released.

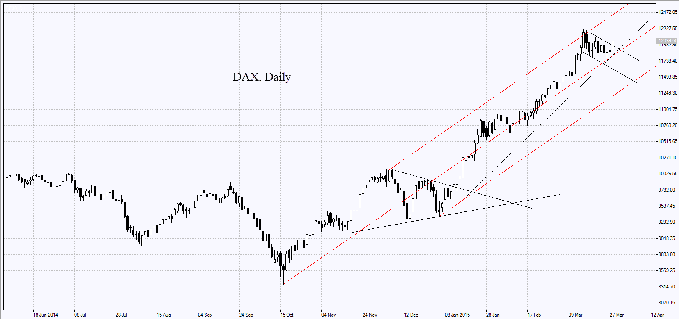

European stocks fell on Tuesday as investors took profits after better than expected economic data from Germany and Spain. Germany on Tuesday issued data showing retail sales in Europe’s largest economy climbed 2.9% in January over December, beating expectations of a 0.3% decline. Employment report from Spain showed that jobless claims unexpectedly fell by a seasonally adjusted 13,538 in February. The FTSEurofirst 300 fell 1 percent but remained close to seven-year highs reached earlier this week. European stock markets have rallied ahead of the launch of the quantitative easing program as investors anticipate that part of the newly issued liquidity will end up in equity markets. Euro slipped as investors anticipate the European Central Bank will announce the start of the bond buying program at its meeting on Thursday. Today at 11:00 CET euro zone Retail Sales for January will be released by Eurostat. The tentative outlook is positive.

Nikkei is falling today as investors took their cue from Wall Street and are booking gains. Exporters are weaker as dollar inches higher against yen, while Sharp tumbled 6.5 percent after S&P cut its credit rating.

Oil prices rebounded on Tuesday with fighting in Libya and tensions over Iran’s nuclear program raising concerns about global oil supplies. Rival forces in Libya carried out strikes on oil terminals and an airport. Prices were also supported by Saudi Arabia’s decision on Tuesday to raise the official selling prices for its oil deliveries to Asia and US by $1 and $1.40 a barrel. The decision indicates OPEC’s largest exporter is seeing signs of stronger demand. Concerns over market oversupply will likely resurface today as investors will be watching closely for the change in the US inventories in the weekly inventory report from the Energy Information Administration. The report is scheduled for release at 16:30 CET.

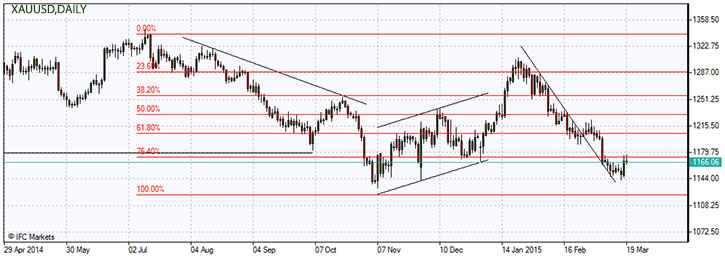

Copper prices fell from a six-week high on Tuesday on speculation that China’s Premier Premier Li Keqiang will announce at an annual meeting of country’s leaders a growth target of about 7 percent for 2015, down from 7.5 percent last year, meaning less demand from the world’s biggest metals consumer. Copper prices rose on Monday after China cut interest rates.

European stocks fell on Tuesday as investors took profits after better than expected economic data from Germany and Spain. Germany on Tuesday issued data showing retail sales in Europe’s largest economy climbed 2.9% in January over December, beating expectations of a 0.3% decline. Employment report from Spain showed that jobless claims unexpectedly fell by a seasonally adjusted 13,538 in February. The FTSEurofirst 300 fell 1 percent but remained close to seven-year highs reached earlier this week. European stock markets have rallied ahead of the launch of the quantitative easing program as investors anticipate that part of the newly issued liquidity will end up in equity markets. Euro slipped as investors anticipate the European Central Bank will announce the start of the bond buying program at its meeting on Thursday. Today at 11:00 CET euro zone Retail Sales for January will be released by Eurostat. The tentative outlook is positive.

Nikkei is falling today as investors took their cue from Wall Street and are booking gains. Exporters are weaker as dollar inches higher against yen, while Sharp tumbled 6.5 percent after S&P cut its credit rating.

Oil prices rebounded on Tuesday with fighting in Libya and tensions over Iran’s nuclear program raising concerns about global oil supplies. Rival forces in Libya carried out strikes on oil terminals and an airport. Prices were also supported by Saudi Arabia’s decision on Tuesday to raise the official selling prices for its oil deliveries to Asia and US by $1 and $1.40 a barrel. The decision indicates OPEC’s largest exporter is seeing signs of stronger demand. Concerns over market oversupply will likely resurface today as investors will be watching closely for the change in the US inventories in the weekly inventory report from the Energy Information Administration. The report is scheduled for release at 16:30 CET.

Copper prices fell from a six-week high on Tuesday on speculation that China’s Premier Premier Li Keqiang will announce at an annual meeting of country’s leaders a growth target of about 7 percent for 2015, down from 7.5 percent last year, meaning less demand from the world’s biggest metals consumer. Copper prices rose on Monday after China cut interest rates.